Warner Bros. Discovery – Assuming Coverage

Lessons from Q1 earnings for media investors

Warner Bros. Discovery (WBD) reported Q1 earnings on Thurs, May 8th. Similar to my writeups on Fubo, Disney and Nexstar, I am assuming coverage of the company going forward and using the Q1 results to flesh out my thoughts on media investing.

Company: Warner Bros. Discovery (Nasdaq: WBD)

Recommendation: I expect WBD stock to Underperform the S&P 500 over the next 12-18 months. I am bearish on the core business and cannot recommend this as a long-term buy-and-hold. However, I would not short WBD given the unpredictability of M&A news. The stock will rise or fall based on how quickly management can divest the linear TV business. While I would prefer an all-cash sale to help pay down debt, an all-stock spinoff is the most likely outcome.

Ownership: I have no positions in WBD stock or options at the time of writing.

Key Q1 Operational Takeaways:

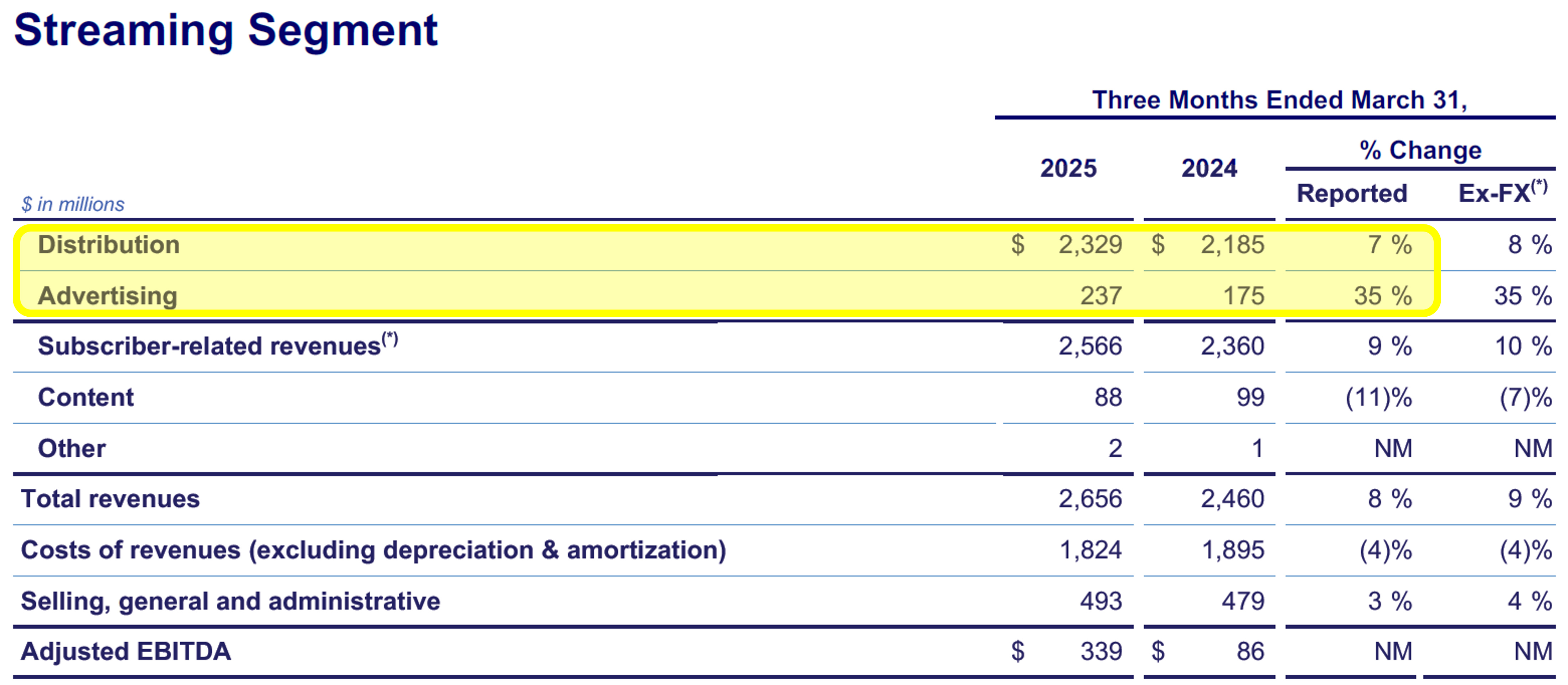

I’m still surprised that WBD, one of the largest owners of cable networks, can’t generate more advertising dollars through streaming. Q1-25 advertising was 9.2% of total streaming revenue ($237M / $2,566M), up from 7.4% last year ($175M / $2,360M). Advertising is still disproportionately coming through traditional pay TV subscribers.

Advertising grew +35% YOY, but it was from a smaller base, less than $200M last year. This growth rate is not sustainable.

Total streaming subscribers grew, both global and domestic. U.S. subs were up +9% YOY, going from about 53M to 58M. Unfortunately, domestic ARPU fell -5.3% from $11.77 to $11.15. WBD said they added more wholesale customers (aka from cable companies) by expanding the distribution of Max Basic w/ Ads. Like Disney, I think Max is also gaining subs from lower-priced bundles. It is ominous that streaming is most successful when it copies the practices that skinny bundles were supposed to avoid.

This might seem counterintuitive, but streaming customers gained through partnerships with cable cos. tend to have a higher lifetime value (LTV) than customers gained through DTC. That’s because while WBD earns a reduced wholesale rate, customers churn less when billed by their cable provider.

International subs grew +38% YOY from 46.9M to 64.6M. This is also unsustainable, as WBD is launching Max in new international markets so you can’t extrapolate this growth.

Despite +8% revenue growth for streaming, it still has low EBITDA margins.

Adjusted EBITDA margins were 12.8% in Q1 ($339M / $2,656M), up from 3.5% ($86M / $2,460M) last year. Streaming will never be as profitable as linear networks. Linear’s Adjusted EBITDA was 37.6% in Q1-25 and 41.3% last year, for context.

And while Streaming Adjusted EBITDA went up +$253M, it still did not make up for linear network decline of -$326M. I do not envision Streaming ever growing fast enough to keep pace with linear declines, let alone driving growth. This is precisely why management wants to sell its linear networks as soon as possible.

The movie business is very lumpy, with revenue correlated to the new release calendar. I will not be covering the Studio segment in detail, because I do not claim to have any insight into how to forecast this better than the market.

WBD loves highlighting its movie studio now, because it allows them to brag about recent box office successes such as Sinners and A Minecraft Movie and their highly anticipated Superman reboot coming in July.

However, with the reduction in the theatrical industry becoming permanent post-COVID, it is unlikely that Studio earnings can make up for declines in the linear networks and the lack of profits in streaming to move the stock higher.

WBD Linear network revenue was down -7% YOY, with declines in both distribution -9% as well as Advertising -12%. Management reported a -9% drop in linear pay TV subscribers, highlighting that cord cutting is accelerating faster than expected.

WBD only generated +2% increase in affiliate rates from cable companies. This combination of falling subscribers and affiliate fee growth less than inflation is why I’m bearish on broadcast companies such as Nexstar (see my Q1 coverage from last week). Everything happening to cable networks will eventually happen to broadcast.

The audience (ratings) at WBD networks declined -27% in Q1, foreshadowing more cord cutting to come. I’m expecting pay TV subscribers to continue declining for the foreseeable future.

The Adjusted EBITDA decline of -15% YOY, which was almost double the -7% decline in revenue. This is a reminder that TV is a high-fixed cost business that structurally cannot hold margin when subscribers leave.

Conclusion + Next Catalysts to Watch

Outside of earnings, going forward M&A speculation will be the only news that really matters for WBD stock in 2025 and 2026. This past Q1 was the company’s first time reporting after reorganizing their divisions to make it easier to break it up into pieces.

Warner Bros Discovery moving towards splitting company, CNBC reports

While no deals have been rumored to date, everyone is expecting WBD to sell or spinoff it’s declining cable TV assets. When you are selling a declining asset with a lot of leverage, time is not your friend. Given the weakening U.S. macroeconomic environment, I think there are higher quality companies worth your investment consideration. WBD could be considered for trading if there is concrete M&A activity.

-Accrued Interest

Disclaimer: The information presented in this Substack is not, and should not be construed as investment advice. Investors should make their own decisions regarding the prospects of any company discussed here, as I am not a registered investment advisor.

IDK, WBD has one of the strongest remaining portfolio's of content/IP out there--super valuable for any of the big streamers/big tech players looking for differentiation. With a 7 to 10X ebitda multiple (from like media M&A comps), we could see a share price of ~15 to ~30. Interesting upside? Or a pipe dream?